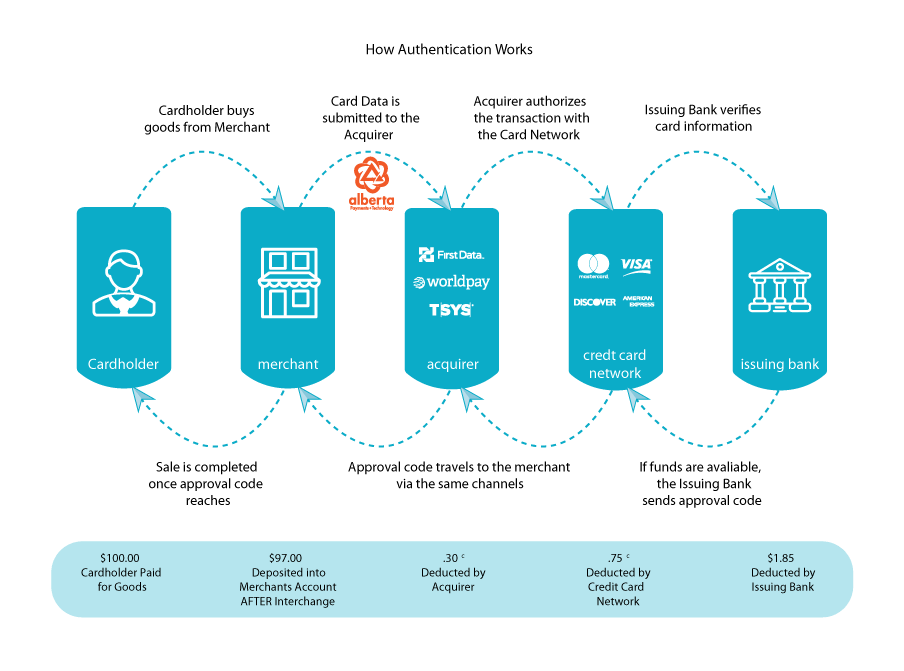

Power to accept credit cards is essential to your business growth, therefore, we work to ensure seamless payment processing which includes next day funds availability. All our terminals are PCI Compliant and EMV Certified. Compatible with most POS systems*

pick your price

pick your price

(Simple, Transparent, and Budget-Friendly)

OR(Tailored Rates for Maximum Efficiency and Savings)

OR(Offset Processing Costs with Transparent Surcharges)

No early termination

We are so confident in our pricing and services that believe in no early termination fee.

No hidden fee

We believe in transparency – what you are promised is what you get

Service you can rely on

We understand the need to attend your queries urgently. Our customer service team is very dedicated and friendly and try their best to help you with any questions related to payment processing. They speak your language too!

Secured platform

Security and fraud prevention is at the core of our business. We make sure all our terminals are EMV certified & PCI compliant.

Alberta POS

Alberta POS PAX S300

PAX S300 Mobile App feature

Mobile App feature PAX S80

PAX S80